Home insurance premiums fell in the last year, even in areas prone to weather-related risks. Photo: RNZ

Home insurance premiums fell across all regions of the country in the last year, even in areas prone to weather-related risks, new Treasury data shows.

The availability of insurance from multiple underwriters also improved in most hazard-prone areas, despite major insurer AA Insurance halting new policies in selected postcodes.

However, areas in high flood risk zones are still attracting thousands of dollars a year in extra premiums, in some cases.

Actuarial consultancy Finity has monitored insurance premiums on behalf of Treasury since late 2022, for a dataset of properties chosen to match New Zealand's natural hazards profile.

The addresses are real but other information, such as property age, sum insured and construction materials, has been randomised so that the 'houses' in the dataset are not real people's homes.

Since October 2023, the monitoring has expanded to include 1710 properties in suburbs around the country that are known to be flood-affected, either by river or surface flooding.

Smaller subsets are used to monitor pricing and availability for other hazard risks, such as landslides.

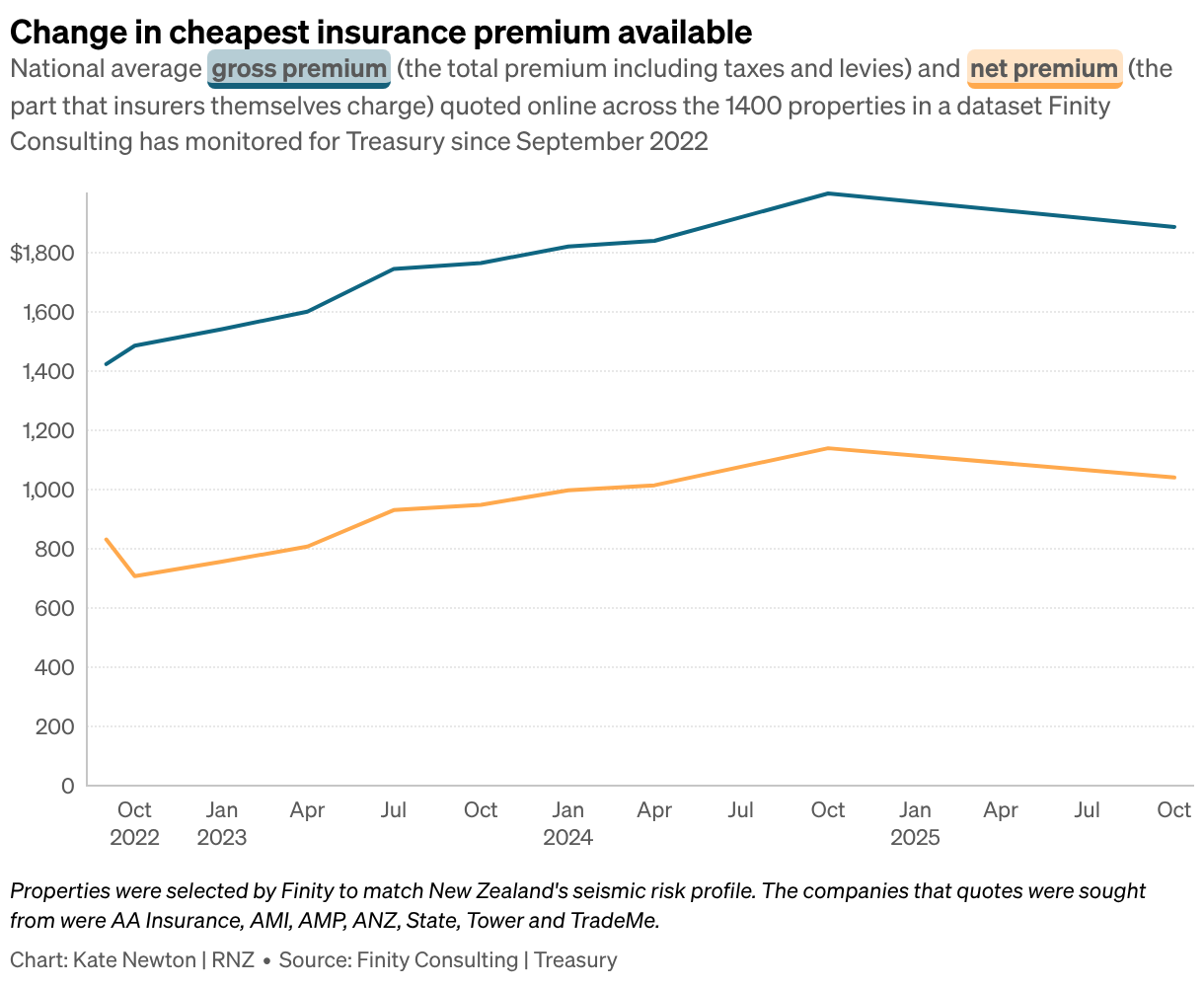

The most recent report, based on October 2025 data but released on Tuesday, showed that premiums had fallen since October 2024 - the first drop in pricing since monitoring began.

That was true for every region in the country.

Nationally, the average cheapest premium available fell from $1999 a year to $1886.

In its report, Finity said that multiple insurers had implemented decreases, driving the average price down.

"New business prices peaked around mid to late 2024 and have been falling since, driven by favourable reinsurance conditions and a benign period of natural perils losses."

The monitoring occured prior to the recent massive storm and flooding in the upper North Island.

Experts have previously warned that insurance will become prohibitively expensive or impossible to get at all for some properties, as the risk from climate change-driven weather events continues to rise.

RNZ revealed last week that AA Insurance has temporarily stopped offering new home insurance policies in Westport because of the town's flood risk.

The Finity data was collected prior to that decision - which AA Insurance informed Buller District Council of in late December.

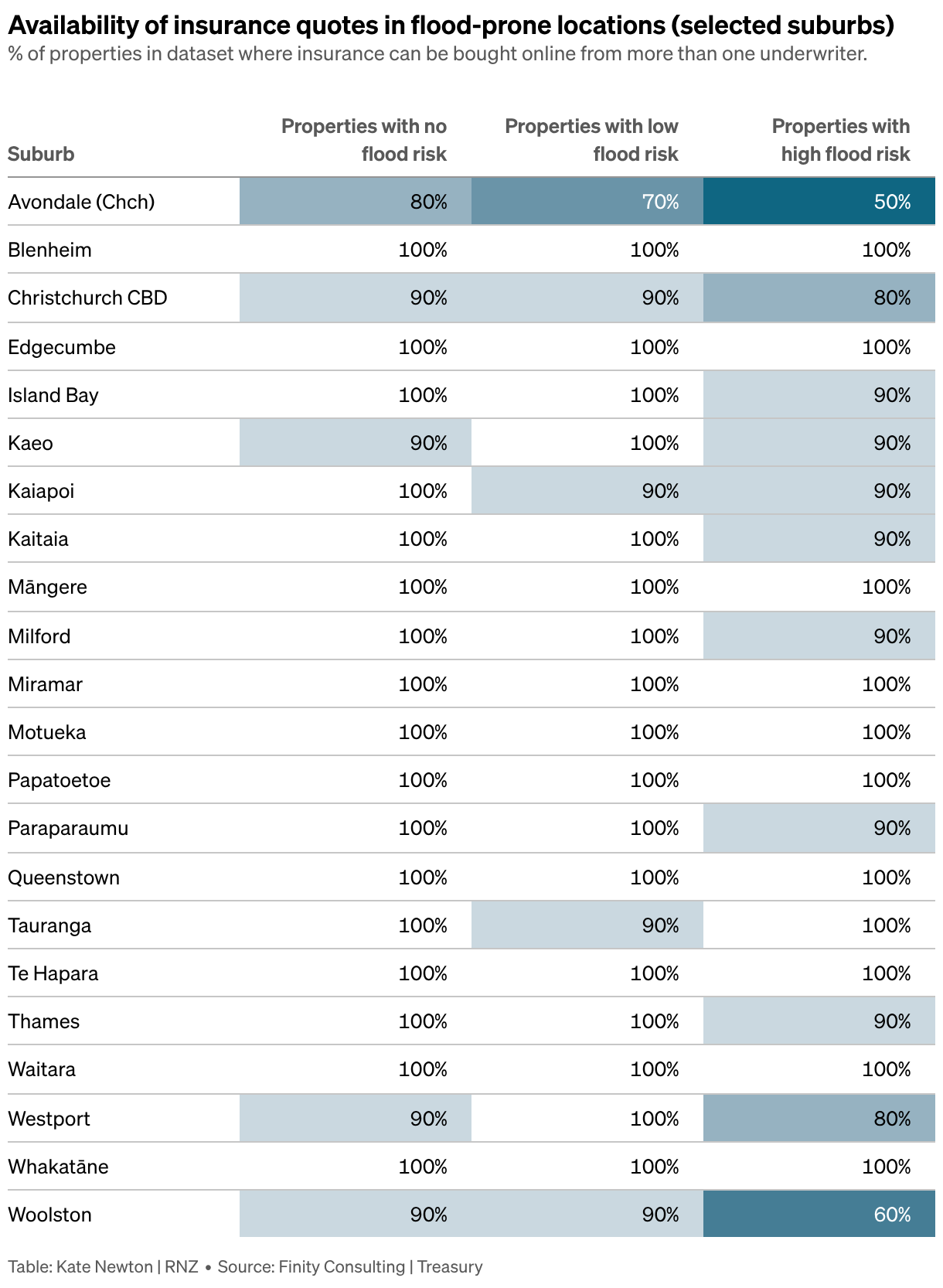

However, there was "clear evidence that many insurers are using flood risk as a driver for their online underwriting criteria", the Finity report said.

"Availability is limited in some high risk flood areas, specifically Avondale, Edgecumbe, Woolston and Westport," the Finity report said.

"For example, the majority of low and high flood risk quotes in Westport only received quotes from two underwriters, with only one [property] quoted by three or more underwriters."

As flood risk increased, availability dropped, the report said.

"High flood risk locations received approximately twice the number of rejections as locations with no flood risk."

For insurers who did provide online quotes, the additional flood premiums were now higher.

The average quote for some of these properties was more than $1000 extra, up to a maximum quote in one case of $9250.

The report noted AA Insurance's approach to new policies in "specific postcodes with very high seismic risk", where a temporary halt had been placed on new policies.

RNZ reported on Tuesday that north Canterbury township Woodend was among those postcodes, along with Rolleston and Lincoln.

The pause, which began last September, also appeared to apply to Blenheim and the neighbouring settlements of Renwick and Seddon.

"Any impact from this restriction on the data shown will be outweighed by the wider increases in online availability in high seismic areas," the Finity report said.

Overall, 95 percent of homes in the seismic dataset could get an online quote from at least two of the four underwriters included in the Finity monitoring (IAG, Tower, AA Insurance and Vero) - a small jump from 93 percent the year before.

That was mostly due to improved availability in Canterbury, central Wellington and the Hutt Valley.

Since the fatal Mount Maunganui landslide last month, landslide risk in New Zealand had earned heightened public attention.

The Treasury data did not show any evidence that insurers were charging additional premiums for properties with a high landslide risk - in fact, these properties attracted slightly lower premiums than the national average.

However, it noted that insurers were paying attention to landslide risk, with Tower expanding its property-level risk-based pricing last year to include landslide hazard.

Tower chief executive Paul Johnston said that had allowed the company to classify 93 percent of its customers as 'low risk' or 'very low risk', with an average reduction of $70 in premiums for those properties.

A 'couple of percent' had been classified as 'very high risk', with increases to their premiums.

A third of those increases were over $100 but Johnston would not say what the largest premium increase was.

For properties facing very large increases, "we're calling them individually and talking to them about that and what we can do", he said.

An Insurance Council spokesperson said it was "important New Zealand takes a long-term view on the risks from natural hazards as we face the prospect of more frequent and severe events due to climate related events".

"We support a government-led approach to mitigate and adapt to the changing climate and an agreed set of natural hazard and climate risk data so we are all on the same page.

"This in turn will help reduce risk, protect communities and keep insurance accessible in the future."

Sign up for Ngā Pitopito Kōrero, a daily newsletter curated by our editors and delivered straight to your inbox every weekday.